Euronext Paris

Euronext Paris

Indices français

| Indices | Dernier | % |

|---|---|---|

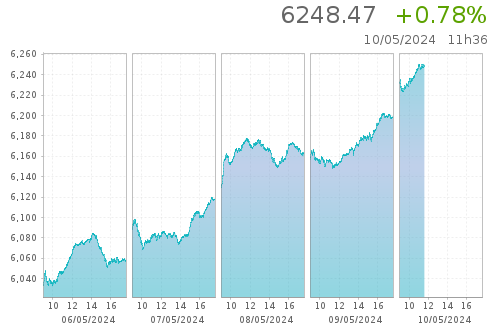

| CAC 40 | 8 016,65 | -0,93 % |

| CAC ALL SHARES | 9 586,62 | -1,20 % |

| CAC NEXT 20 | 10 973,12 | -0,88 % |

| CAC SMALL | 11 659,82 | -0,81 % |

| SBF 120 | 6 055,72 | -0,93 % |

Indices EU

| Instrument-name | Last-price | Day-change-relative |

|---|---|---|

| EURONEXT 100 | 1 504,93 | -0,72 % |

| CLIMATE EUROPE | 1 900,84 | -0,31 % |

| LOW CARBON 100 | 161,34 | -0,17 % |

| NEXT BIOTECH | 2 062,85 | -1,34 % |

| ESG 80 | 2 047,40 | -0,88 % |

Taux de Change

| Instrument-name | Last-price | Day-change-relative |

|---|---|---|

| EUR / USD | 1,07344 | +0,33 % |

| EUR / GBP | 0,85761 | -0,10 % |

| EUR / JPY | 167,011 | +0,56 % |

| EUR / CHF | 0,97946 | +0,07 % |

| GBP / USD | 1,25165 | +0,44 % |

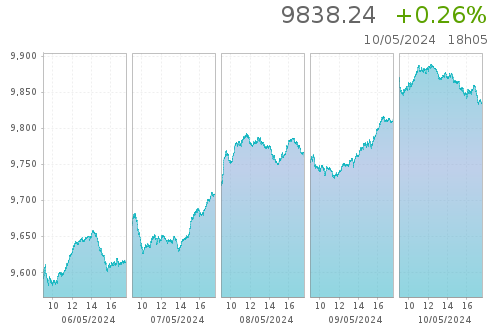

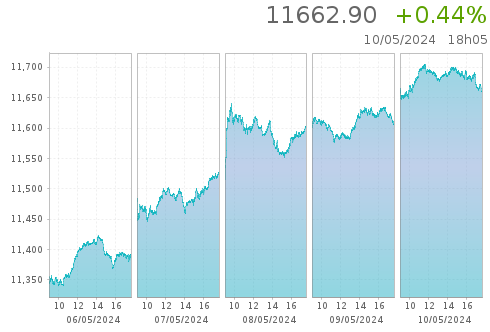

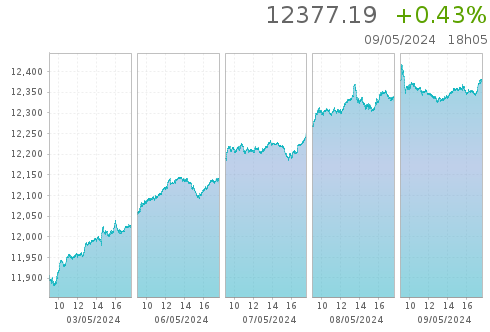

Indices Francais

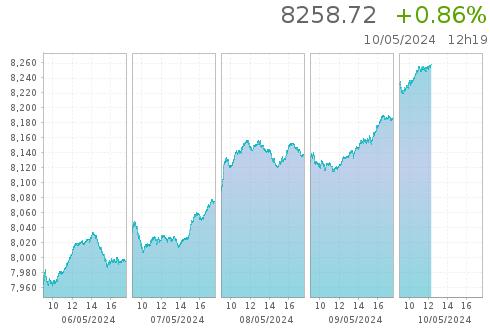

CAC 40

CAC ALL SHARES

CAC NEXT 20

CAC SMALL

SBF 120

Marchés au comptant

Marchés dérivés

Communiqués reglementés

Euronext Paris

Pour plus d’information sur Euronext Paris

Visitez la section dédiée sur Euronext.com